Hello Guys. I’m Angus Scott from ElitePersonalFinance.

Thanks for watching.If you are in the unfortunate situation of having bad credit and need money, watch this video carefully. The bad credit loan market can be a very dangerous place. Many people don’t know what they are doing and end up getting costly payday loans. They end up paying costly interest rates, and worse, some end up getting into a vicious debt cycle and destroy their credit rating even further. This does not have to be the case. There are many more options than payday loans, even if you suffer from really bad credit. In this video, we’ll discuss all of these.That’s why we decided to create this complete guide on bad credit loans. Here we will give you all the options and the steps to take if you suffer from bad credit.So, please watch this video to the end. I’ll guarantee you’ll probably discover many things you didn’t know.

Before we move on to these things, I just want to make sure you’ve watched our previous video. There, we discussed how people with bad credit could get approved on a legitimate personal loan. That’s absolutely possible. And this should be your step number one. If you haven’t watched those videos do that first, then take a look at what I’m gonna discuss here.

Make sure you watch this one:

And don’t worry, there’s a link below to that video.

And make sure you check out this link – again, we’ll have it below – where you can shop around in the marketplace where we have shown you all the best options for you, side by side.

Now, unfortunately, there are cases when people, because of their bad credit, can’t get approved for a personal loan; or they get approved for a very low amount that doesn’t work for them, or they don’t get offered good terms at all.

So what should you do? Go and get a payday loan? NO!

Don’t give up!

As you already know, we work very hard to uncover all the options available to you that are times better than payday loans and auto title loans to help you get a legit loan even if you have bad credit.

So, again, watch the video very carefully. There is a lot of crucial information you need to know!

Secured and Co-signer Loans

Even if you have bad credit, you could still qualify for a secured personal loan – also known as a “collateral loan” or for a “co-signer loan.”

For these, you obviously need what’s called ‘collateral’ – that’s something you offer up to the lender as security against the money you’re borrowing. Now, typically, collateral is your car. However, some people add their savings.

First things first, if you’ve got money in a savings account, it’s obviously cheaper to use that money than get a personal loan that charges interest. However, if you need to hang on to your savings or need more money than what’s in your account, some lenders will make secured personal loans with savings accounts or certificates of deposits as collateral. Be aware, though, the terms of any loan like this usually mean you won’t have access to your savings account or a Certificate of Deposit until you repay the loan.

So, here’s the important part. When you add collateral on your loan, whether it’s your car or your savings, or you add a co-signer on your loan, what you’re actually doing is lowering your credit risk for a lender. And what that means in practical terms for you is that:

You’re more likely to be approved for a loan;

You’re more likely to be approved for a higher amount and;

You’re more likely to be offered a much cheaper interest rate.

And this is even if your credit score is bad.

See, in each of these cases, lenders won’t then just review your credit score, your income, and debt-to-income ratio, but they’ll also add into the mix the positive value of the collateral or the cosigner loan factors as well.

For example, with a secured loan, the likely approved amount would be calculated based on the collateral value you’re adding in. At the same time, obviously, be aware that the lender will not approve a loan amount that they believe would be impossible for you to pay back.

With a co-signer loan, the lender will evaluate that person’s creditworthiness. So choose that person carefully. They could make all the difference, especially if they have a better credit score.

The bottom line:

The great news is that these things really do work. Many people who suffer from bad credit get approved and have significantly cheaper rates and much higher loan amounts. But, there is a ‘but’ here. These loans come with some risk to you.

On a secured loan, you risk losing your collateral if you stop paying.

On a co-signer loan, you risk your friendship with that person.

In both cases, if you stop paying, you also put your credit score at risk.

So, our advice? Investigate and use these loans, but only if you know what you’re doing. The golden rule is only to get one of these loans if you are sure, and I’m mean sure, you’re gonna repay it on time.

And now:

Who offers the best-secured loans?

Well, you can usually find these being offered by most banks, credit unions, and online lenders. I’ll come on to give more info about these shortly.

On the banking side, Wells Fargo and US Bank are amongst the most popular banks in this business.

For credit unions and online lenders, there are a lot of these. And we’ve made looking for the right one for you a lot easier.

You can visit our page, where we list the best-secured loans.

And we keep this page regularly updated, showing you the best lenders at any given time.

Now, coming up next is something that’s an exciting development…

But before that, let me ask you a few questions.

What’s your experience with secured and cosigner loans?

Which lender would you recommend to us?

How much do you lower your APR on secured vs. non-secured loans?

Please post a comment below this video. We appreciate it.

Credit Unions and Banks

Credit unions and banks are great destinations for people looking for personal loans.

But first, let’s start with the bad news.

If you have bad credit, banks are the hardest to get a personal loan from. By their very nature, Banks prefer to work with people with good credit scores. And even then, those with good credit and high incomes can still be required to secure their loans or add a cosigner. This just happens to be the current situation with banks.

So, if you want to try banks, go for it, but don’t waste too much time …

And I’ll let you into a badly kept secret… banks don’t have the interest to offer personal loans. They make much better money from credit cards, which are much more profitable for them, so people with bad credit have little chance.

So, instead, let’s talk about credit unions.

Now here, you have a real chance.

Credit unions do approve people with bad credit.

Some quick facts about credit unions:

Credit unions pay more attention to factors like your income, debt-to-income ratio, your recent financial transaction history, your workplace, and so on instead of your credit score.

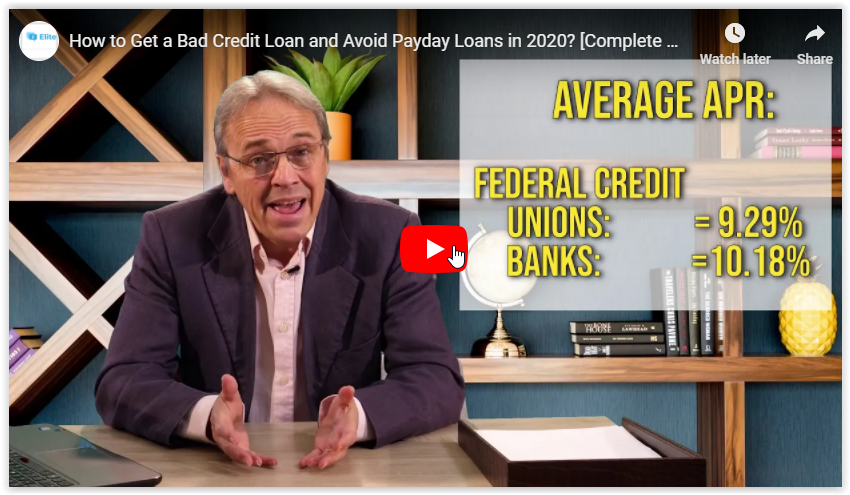

Over the past five years, according to data from the National Credit Union Administration, federal credit union loan APRs on three-year loans have averaged just over 9% whilst banks charge just over 10%.

And according to economists from the Credit Union National Association. State-chartered credit unions have charged an average APR on loans of 11.43% over the past five years.

And one final point worth noting, their Loan officers will help you. He is willing to consider factors beyond your credit score.

These facts make them a great destination for people with bad credit.

As you can see, credit unions even beat the banks in terms of APR.

As always, we have an up to date list of the largest credit unions here:

and again, you can find this link in the description below.

Another great thing about credit unions is that they can offer loans to surprisingly large amounts, some of them even up to $100,000. Credit unions cap their APR at 18%, which is pretty favorable for anyone with bad credit.

Credit unions also have a cash advance option for people with terrible credit, also called payday alternatives (PAL). These are quick cash options, typically $500 to $1,000, with an APR capped at 28%.

Now, if you watched our last video about payday loans, you’ll understand why we’re suggesting you look at these instead. I don’t think it’s hard to see the benefits of 28% APR against 400% on a payday loan. You get the idea…!

Alternative Payday Loans

Now, what about PALs.

As of December 2019, credit unions started to offer a new PAL type, called a PAL II.

What I suggest you do straight after this video takes a look at this page – and again, you’ll find it in the description below.

On this page, you’ll be able to see in clear detail the difference between each of them, and it’ll help you decide which ones you want to look at.

So what you’ll find is that PAL IIs can offer up to $2,000, repayable over 12 months. And they’re fast – as soon as you become a member of that credit union, you can take out the loan immediately.

But – and there is an important ‘but’ here – before you dive in there, there are a few important things about credit unions you should know.

Credit unions perform what’s called a “hard credit pull.” When we talked to you about shopping around with personal loans – DON’T do the same with Credit Unions. When you’re looking at personal loans, they only make a ‘soft’ inquiry on your credit score, so it doesn’t matter how many applications you make. It doesn’t impact your score.

But with credit unions, this is not the case. The ones we mark, like here, make a ‘hard’ inquiry, which means every time you make an application, it’s noted on your credit score and deducts points from it. So, imagine if you went and applied to 10 or 20 credit unions at a time. What’s gonna happen to your credit score? Just the act of applying will seriously damage it further.

So, what’s the solution?

Some credit unions list their loan requirements on their websites, so take a look and check whether you meet them. That way, you can quickly find out if you’re likely to be rejected without actually going through the application process. But the best tip that we can give you is actually to pick up the phone and call them. Describe your financial situation and ask about your chances of being approved. Loan officers will help you. They’ll be honest with you and give you a clear indication of whether or not it’s worth you making an application.

Some other points you should also take into account when choosing which Credit Union you want to go for:

Firstly, Credit unions require you to become a member and, of course, with that charge monthly fees. So make sure you check out what those monthly fees are.

And secondly, Credit unions have fewer branches than banks. This may or may not be an issue for you.

But that’s why our final tip on choosing which credit union is this:

When you apply for a loan or any other product with a credit union, check all their offers – all types of loans, credit cards, savings accounts, and so on because it’s much better to work with one credit union and get all the financial products that you may ever need from one place. All credit unions want to make you a regular customer, and they incentivize you to do this – which basically means you end up getting a better deal.

And before we move on with the next section, let me again ask a few questions:

Tell us about your experience with credit unions and banks.

Have any of you being approved with low credit? What APR?

Credit Cards for Bad Credit

So, what about credit cards?

Credit cards for anyone with bad credit is a big topic that we’ll cover in more detail in another video.

But in the meantime, let me just give you a few important points you should bear in mind.

Most credit cards for bad credit are secured. In some cases, the security deposit that the issuer wants from you could be equal to the card’s actual limit, which basically means you’re paying a high interest rate to borrow money that you, in theory, could already use for nothing.

Also importantly, most credit cards perform a hard credit inquiry in the application process. So again, on these, ignore our usual golden rule of ‘shop around’ – be very selective and apply only if you are sure that you meet the criteria and you will be approved.

So, if you do want to apply for a credit card, first of all, read their application criteria very carefully and see whether you meet them.

Next, most credit cards have a pre-approval tool. This allows you to enter your details and see whether you actually have a chance to qualify.

Then, you should call the credit card issuer and talk to them. This is a long and exciting topic because there are many precious tips that we can give you on how to talk to them and what to tell them exactly. Based on how you speak to them, we can teach you how to qualify for a credit card even where you don’t meet the criteria. But you’ll have to watch our next videos for that.

And last. Credit cards are a great credit-building tool. And if you subscribe to our channel, we’ll teach you the tricks of the trade on building your credit score using credit cards only.

But again, as I said, this is a very long topic that we’ll cover in our next videos.

And maybe this is the moment to lay it on the line about us. We operate a trendy and successful website where we’ve been giving people like you a handy tool to make smart financial decisions – saving countless people from getting into a real financial mess.

So, producing these videos is a new direction for us – we wanted to make it more personal, talk directly to you guys, and get a real understanding of how you feel about these products and your stories. This is your chance to talk to us. Ask us questions!

So, please subscribe. Thanks for supporting our channel.

Loan Apps

So, next, I want to talk about loan apps. These are still relatively new types of loans but definitely gaining in popularity.

This is a fast-growing market, and as always, we’re keeping tabs on this because it does seem to be gaining the interest of many people – so what we’ve done is put all the information together for you here.

Many loan apps offer fast cash very cheap, and believe it or not, some of them even offer zero interest rates. Hmm. So, where’s the catch? I hear you ask!

Some of these apps have membership fees, but these fees are actually not so high.

For example, with Dave, you can get access to $200 instantly at any time if you pay only $1 per month.

At Vola, you can get $300 if you pay $4.99 per month.

Now, the cons of these apps are that they offer relatively low amounts of cash. But the approval is speedy. Most of them don’t even check your credit score – but they do check your past financial transactions.

Our advice? You should definitely check these out. Most of them have become extremely popular, and our gut feeling is that these are potentially gonna be the next big thing in small loans. With the increasingly digital world and our lives being taken over by apps, we’re not surprised by this as the loans market is always innovating, it’s very competitive, and because of that, lenders are always looking for new ways to grow – and this could be to your advantage.

Don’t forget, visit this page – link below again – where we will always update you with the latest in the business at:

But, whilst all sound great, do be careful – there are scams out there. Many predatory payday lenders noticed the growth in this niche and started to develop cash apps themselves. Note that these apps are nothing more than your everyday, regular payday loans dressed up in a nice shiny new suit … ok, some of them may be slightly improved to try to show they are different from payday loans, but you get the drift.

And overall, most of them are still very expensive and pretty much the same as your payday loan.

We do NOT post any of those.

Now it’s time to ask you about your opinion on loan apps. Is there an app that you have something positive to say about it? Or you have been scammed by predatory loan apps. Let us know, and other viewers of this video know. Post your comment below.

Loan Comparison Sites

Loan comparison sites ask you to enter your details one time on their platforms, and then they send this information to many lenders in their networks. These sites really can save you time and help you actually find the best loans available for you very fast and easily.

Credit comparison sites don’t make money from you, which means your loan price won’t be affected if you get the loan through them. Instead, they get a percentage from the lender if you end up getting a loan from them.

You lose nothing in trying – particularly as the credit pull on most of these is a ‘soft’ one. And most of these comparison sites make sure that all lenders that receive your information will NOT perform a hard inquiry. But you have to make sure that this is true.

Let’s go to SuperMoney, one of the largest loan comparison sites that we recommend trying.

As you can see, there is clearly written:

‘Checking rates won’t affect your credit score.’

Which is a good place to start.

Alternative Payday Loans

Alternative payday loans work great for people with bad credit. Most of them are even no credit check loans, making them a great place for terrible credit people. Now don’t stress about the fact that you read the term payday loan in their name. Alternative payday loans are different from payday loans. In fact, they were created to help you avoid payday loans.

Very easy and fast approval for really bad credit!

But …

They are still expensive.

If we have to define them, they are between a payday loan and a personal loan.

Now personal loans are usually relatively large loans, even up to $100,000, paid in installments. Their APR is capped at 35.99%.

Payday loans are typically for small loan amounts, say around $500 to $1,000, paid off in one installment. Their APR is very high, and according to CFPB, it averages around 400%.

It’s more than obvious that the gap between these types of loans is huge.

Alternative payday loans are those that actually fill this gap.

They are everything that is between personal loans and payday loans.

Their typical amount is between $500 to $5,000.

Their APR is between 35.99% to 400%.

Now, there are exceptions to these values. I’m only giving you a basic overview.

Next, alternative payday loans also have many benefits against payday loans.

They can be set to be repaid in installments.

They are times cheaper than payday loans.

They actually work with you to help you boost your credit score. If this happens and you pay them on time, you should expect a discount and better terms in the future.

Okay, we have a full guide on our site about alternative payday loans for those interested in learning more about them from us.

Now you should probably ask, do we actually recommend them.

The answer? Well, yes and no.

They really can save you from payday loans, but they are still very expensive.

So, use them only if you don’t have any other option than a payday loan.

But again, try everything, guys. Many people think that they have no other options. And they are wrong.

Final Tips

The most important thing in your financial life is your credit score. People with bad credit who have a loan should immediately start working on that credit score from the day they take that loan. If you pay that loan back on time, your credit score will rise within months because most legit lenders report your activities with credit bureaus. At the same time, you should also try everything else possible to boost your score.

And then, of course, if this happens, you should instantly apply for refinancing with something a lot cheaper. It’s not rocket science, but so many people don’t think to do this. And it could save you a lot.

So, what do you do? First, go to your current lender and update them on your credit score changes and ask if they have any better options for you.

Second, again shop around with all lenders. Try credit unions, banks … but don’t forget they perform a ‘hard’ inquiry, so ask, don’t apply.

And repeat the same process every 3 months.

So very soon, your payday loan with an APR of 400% will turn into an alternative payday loan with 100% APR.

Then your alternative payday loan turns into a personal loan for bad credit at 30% APR.

Your personal bad credit loans will turn into a personal loan with good credit with rates as low as 5% to 10%.

Do you get it?

The bottom line:

This technique can save you a lot of money on interest and help you set better repayment plans if you use it correctly … So the key is – really work and boost your credit score and shop around, as we’ve explained.

And finally, to wrap up… a shocking fact…

Check your credit score now

Do you know how often credit reports contain errors? According to a study by Experian, around 30% of all credit reports contain at least one error.

That is a lot!

So, step number one, check your credit score now, review it for errors, and if you find one, report it straight away. Your credit score should boost very quickly, usually within a month. This is the easiest and 100% legit way to boost your credit score fast.

The really shocking part is many people know this fact, but they still don’t check.

The fact that 30% of credit reports are basically wrong means that at least 30% of people haven’t performed this check.

Let’s go back to our tip number one – if you suffer from really bad credit, try to avoid getting a loan at all. But, even if this doesn’t work for you, here is what we recommend. Wait, work on your credit score and when it approves, get a cheap personal loan. People with bad credit don’t complain of a lack of offers.

Try to decrease the loan amount. If you think you want $1,000, reconsider your budget carefully, and I mean to be ruthless with yourself. Do you really need that much? Maybe you could actually get away with only borrowing $500.

But … don’t go too far that way.

If you do end up borrowing too little and find yourself having to cut expenses you genuinely can’t do without, or, worse, it makes it harder for you to make your loan repayment schedule, and then you’re risking getting yourself into an even worse situation. You then prevent yourself from refinancing with a cheaper loan and, in turn, just end up making your credit score even worse – and once again, paying even higher rates.

So, don’t get more than you need, but do get a few extra bucks over to protect you in a bad situation.

And the moment that you get a bad credit loan, even if it is a payday loan, change your finances accordingly, and your only focus after that should be to repay that loan as fast as possible.

Big NO! Don’t get expensive loans like payday loans for things like travel, clothes, and unimportant things.

Get these loans only to fill important budget gaps, or you have no other options… which we again wanted to tell you is almost not possible.

A few important facts to wrap up

The lending market is constantly changing. There are always:

New lenders, so the competition’s constantly growing.

Many lenders just keep improving their terms.

And the market is always innovating: we’ll keep seeing new, innovative loan products hitting the market like, for example, those loan apps that didn’t even exist until recently.

So, you should always keep your knowledge updated on what’s out there.

And even if you’re currently paying off a loan always, always keep reviewing new options and see if you can refinance with something cheaper.

This is an ongoing process that shouldn’t stop.

We at ElitePersonalFinance will help you in this process by keeping you updated all in one place – our marketplace.

One of the largest, free financial marketplaces for all financial products, all in one place. So seriously, use us!

And now, let me ask you a few questions. The best part for us!

We really appreciate your feedback because we learn a lot from you – people who give us your honest feedback.

In fact, in most cases, we’ve actually learned more from you than we have from so-called financial experts, gurus, and so on!

So, my questions to you are:

What was the lowest APR that you’ve been offered with bad credit: from online lenders, credit unions, banks? Give us some names and values.

If you’ve had bad credit and have been turned down for an unsecured loan or maybe offered ridiculously high APRs, were you then able to get a secured or a cosigner loan at a reasonable rate?

What do you think about PAL IIs? Did you know about them, and have you tried to ask your credit union after you learned?

What do you think about alternative payday loans?

And finally, have we missed anything in this video? Don’t be shy; share where people should go for a bad credit loan!

Just use the comments below to share your thoughts with us.

And don’t forget to please like and subscribe to be the first to watch our next video.

Incidentally, if you have your own site or blog and want to embed our videos, please feel free to do so – you’ll find the link to our channel below. That way, you can have our financial advice boosting your own material if that interests you.

That’s it, but we’ve got some really interesting stuff in our next video you should listen to, so please don’t forget to subscribe. And don’t forget to tell us what you think right now in the comments below.

Thanks for watching, this is Angus for ElitePersonalFinance, and I’ll see you next time.

Best Loans is Alaska

Best Loans is Alaska