Are you looking to buy a new car?

Need to finance it?

You are not alone. The majority of auto purchases are financed, amounting to more than $1 trillion in debt across the nation.

That said, sometimes financing is a ‘necessary evil,’ and you have no way around it. You might even have financial reasoning for your choice to finance. Regardless, it is important that you understand how your credit rating can affect your auto loan.

What Credit Score is Needed to Buy a Car?

For those who want to get a credit report (not exactly FICO score, but similar to it), we recommend CreditSesame, because it is totally free and provides reliable identity theft protection. Get your credit score in minutes.

Anyone can buy a car, but you must jump through some hoops and pass a few hurdles on financing one. The roadblocks that get in the way are greater when your credit score is weaker. If you have a low FICO Auto Score, you can expect that many auto lenders will either reject you or give horrible loan terms.

Do not let that get you down!

There is no such thing as a ‘lowest credit score to buy a car,’ so despair is unnecessary. You can qualify for auto financing, even if you have unforgivable credit problems and even without cosigner support. Heck, bankrupt borrowers who had their old vehicles repossessed have been able to qualify for new car loans. As long as your income is in order, most online car loan providers are willing to bend the rules a little to ensure you get approved.

How Your Credit Score Can Impact Your Car Loan

Your credit rating’s strength will dictate your likeliness of approval for the loan and influence the interest premium you pay. Low borrowing status will net you some of the worst rates and terms, as the car loan industry is not federally regulated with maximum rates. Instead, the lender is in charge of determining your interest rate, and this comes down to assessing the purchase and the borrower’s credit file.

The lender will assess factors like your credit availability, any past delinquencies, and how recently you applied for other credit lines. The auto lending company could also ask about your job history, income, and other variables. Most of this will influence whether you get approved in the first place and the maximum you can borrow. You do not need a particular credit score for car loan approval, but having a higher score will make your loan more affordable.

While there is no such thing as a minimum credit score for a car loan, it’s important to mention that you can still get rejected for having a low credit score. This is even more likely when dealing with big-name players, like Capital One Auto Finance.

If your credit rating is horrid, fix it before applying or find an auto lender that accommodates bad credit borrowers. There are some services with as high as 99% approval for bad credit applicants, so there is a good chance you will find a lender.

Comparing Interest Rates by FICO Score

For comparison purposes, we will evaluate FICO scores ranging from 500 to 850 as this makes up the majority of potential borrowers. The dollar amounts are calculated assuming a $25,000 principle on a 60-month new car loan in the chart provided below.

| FICO Score: | APR: | Monthly Cost: | Total Interest: |

| 500 – 589 | 14.723% | $591 | $10,467 |

| 590 – 619 | 13.637% | $577 | $9,621 |

| 620 – 659 | 9.372% | $523 | $6,409 |

| 660 – 689 | 6.81% | $491 | $4,477 |

| 690 – 719 | 4.593% | $467 | $3,028 |

| 720 – 850 | 3.281% | $452 | $2,141 |

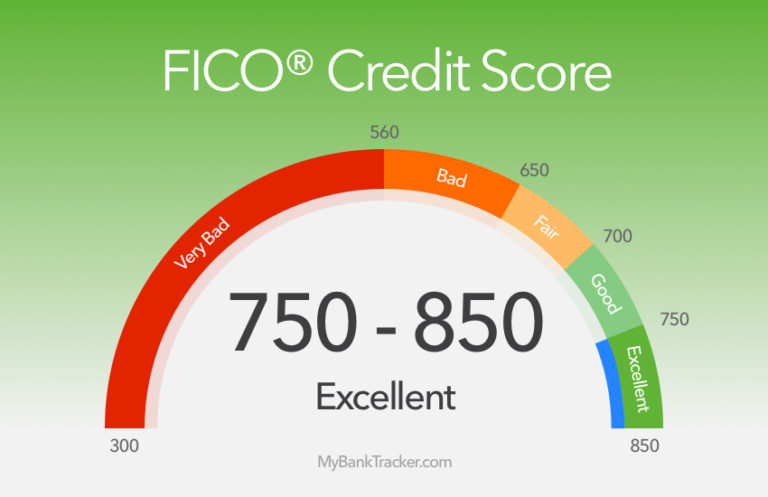

As you can see, the total cost of a $25,000 auto loan could vary by as much as $8,326 in just five short years. This means it makes sense for borrowers with low credit scores to work on their credit ratings before getting financing. For best results, you should aim for at least a FICO score of 660 before applying for a new car loan.

What’s Your Credit Score?

FICO is the most common credit score model that gets used by lenders. Yet, gaining access to your official FICO score is not easy nor affordable. It might be free for your lender to pull, but you could find yourself paying a sizable amount to keep up-to-date with your FICO score.

This is why you might want to consider taking advantage of the identity theft protection service. Not only does it help keep your identity safe (and free from credit destruction!), but with it, you get regular credit score updates under a similar rating algorithm. It also comes at the same cost as FICO’s monthly plan, which gives you credit monitoring but not identity theft protection.

Again, if you cannot manage at least a 660 FICO score, you might want to improve your credit score before applying for a car loan. There are still many lenders that will accept you, but there is a much greater chance that you will overpay on interest costs. Of course, you can get a car loan with a 600 credit score, but the premiums and total interest will be much higher than it is for a borrower with strong credit.

How to Build Your Credit Fast?

Is your current FICO score pretty low in the charts? If so, you should take the initiative and try to build your rating up for at least a few months before inquiring about an auto loan. This is especially true if you have any new accounts opened in the past 3 to 6 months.

When attempting to improve your credit score for car loan purposes, keep each of the following points in mind.

Credit Report Errors

Misinformation on your credit report can attribute to a lower credit score calculation. You have the right to dispute any entries on your credit report that you deem invalid. Whether the transaction was not authorized or the amounts are inaccurate, you can request removal by the three credit bureaus.

Credit report errors are more common than you think. In 2013, the FTC found that 5% of American credit reports contained errors resulting in your credit score being 20 or more points off. If you are one of the lucky ones who hits the 1 in 250 odds, your credit report correction will net you a score change of more than 100 points.

With that said, you can get your free credit report from each bureau through AnnualCreditReport to check for any mistakes. If any errors are found, go to that bureau’s website to dispute them. You should review your credit reports before taking action to see if there are any ‘easy outs’ to boost your score up.

Damages Caused by Debt Charge-Offs

If a charge-off happens to a credit line, there will be a steep decline in your credit rating. This takes about 180 days of late payments to trigger. If you are running behind on any of your debts, make sure to pay them off before borrowing more. Not only does the effort to pay outstanding debts look good, but it also safeguards your score from dropping further before you actually apply.

Remember, a ‘charge-off’ does not happen until the late payment period is exhausted. This is six whole months where you have the ability to get yourself back above water. As the charge-off is one of the biggest ‘nails in the coffin’ to your credit score, it should be avoided at all costs. In short, though you have been late with your payments, “late is better than never” in this case.

Understand The Changes in FICO Score 9

FICO Score 9 focuses a lot on relieving the negative impact caused by medical debts. Understanding how the rating calculation differs now makes the right moves to increase your score.

One significant change to note is that medical collections debts are not as influential as non-medical collections debts. In previous years, owing for a medical procedure could cause your credit to go into ruins. Now, the effects are minimal so long as you do not have any outstanding non-medical collections debts. As such, you can allocate your funds towards other debts first before worrying about your medical ones.

Understand How Auto FICO Scores Work

There is no telling which version of the FICO credit score that your prospective lender will use. A regular algorithm may be chosen, yet the lender might also turn to the specific auto lending model administered by FICO themselves.

FICO Auto Score 8 is the main FICO score algorithm used by car loan providers to determine an applicant’s creditworthiness. FICO gave each of the three credit report bureaus a unique way to calculate Auto Score 8 for their users. This means your rating will vary depending on your credit reports’ information and how those bureaus factor it. Most will find the difference to be no more than 5 to 10 points in either direction between agencies.

Outstanding Debts

The amount you owe makes up for around 30% of your FICO score calculation. This falls second to ‘Payment History,’ which amounts to 35% of your credit score. This means you should try and pay off as much as possible before trying to borrow again. If you have a substantial amount of outstanding debt, the more you pay off, the better your FICO score will get.

Remember, score fluctuations from debt repayment can take a few months to take effect. If you plan to boost your score before applying for a car loan, you should set aside at least 3 to 6 months to see it through. Otherwise, you might use just a few months before your score puts you in the position to save a substantial amount on interest payments.

Should I Waste Time and Money to Boost My Credit Score?

This is the hard part. It’s impossible to say whether you should take the time to build your credit or take the leap with the current rates and terms an auto lender will give you.

Again, we fix in on that 660 FICO score rating for a reason. It’s seen as the ‘benchmark’ number that classifies an individual as an ‘above average’ borrower. As such, you should wait till you can get your FICO Auto Score 8 number a little above 660. If you rely on a different credit rating mode, you might want to make a buffer and shoot for a 680 to 700 score range instead.

Why Do We Recommend a 660 FICO Score or Higher?

As you saw in the chart earlier, the amount you pay out in interest varies greatly based on your credit rating. You could pay just over $2,000 with excellent credit, or well over $10,000 with poor credit. Yet, a 660 FICO score puts you at only under $4,500 in total interest over the course of a five-year new car loan on a $25,000 principal balance.

This appears to be the ‘sweet spot’ as moving your score higher involves a lot of work and gives a little reward. If you are under a 660 FICO score, boosting it up from the next range below will amount to nearly $2,000 more in savings. This is an easy jump to make as it involves moving from the 620 to 659 range into the 660 to 689 range.

If you have a much lower score, whether between 500 to 589 or ranging from 590 to 619, any approved loans will be at astronomic interest rates. These two score ranges factor to almost the same interest totals; a score between 500 to 589 will cost $10,467 in five years, while a score ranging from 590 to 619 will still run $9,621 in interest.

So, there is no reason why you should bother applying for an auto loan if your credit score is that low. You would be better off taking a few months to get your outstanding debts paid off.

You could drop a few thousand on that and clear those debts for good, or throw it away to more interest payments. The smart play won’t just save you money. It will also secure you a better credit score. With that said, what would you prefer to do?

What Else I Can Expect with a Good Credit Score

Yes, it will not be hard to finance a new Ford or Toyota if you have a great score; of course, having a better score also means getting a better interest rate. This makes your loan cost less in the end, which makes it less difficult to pay off.

After you buy the car, the auto loan is only one of the many recurring expenses you will face. The two other major expenses are your fuel and insurance. While your gas consumption is hard to control, you actually have a bit of influence on your insurance costs.

Well, your credit score does.

Consumer Reports blew up the myth claiming that credit scores do not impact insurance premium costs. This full-detail expose suggests that, in New York alone, someone with good credit would pay over $250 more in a year than someone with excellent credit. Interestingly enough, the difference varies by state, and in California, you would not have to worry about such a premium.

The same report found that deductibles on your auto insurance policy fluctuate along with your credit score. If you have a weak FICO rating, you can expect to pay more for a deductible in the event of an accident than someone who has excellent credit. While this seems unfair, the truth is that an excellent borrower would be more inclined to pay for small repairs out-of-pocket to prevent an insurance premium jump.

Find Your Insurance Premiums to be Unfair?

You have the right to request an exception to the rules based on the claim of abnormal life circumstances. This should be done if your credit rating has a serious impact on your coverage. Whether it gets you denied, causes higher premiums, or leads to lower coverage total, you have the right to request that they work around the penalties to serve you better. Further, you can dispute an insurer if they cancel or reject your coverage renewal because of your credit rating change.

For best results, shop around for the most reasonable premiums and coverage terms you can find. Although, if you have poor credit, you might want to consider boosting your score first. Not only does your credit score fluctuate a $25,000 loan repayment total by over $8,000, but it can also vary insurance premiums by more than $1,300 per year.

That said, you might find yourself getting the same horrible quotes from various lenders. If that happens, take action to reduce your insurance costs instead of forking the premium. This is easy to do if you have a real-life circumstance that justifies your weaker credit status.

For example, if you just went through a divorce and your shared debts ruined your credit rating, then you might qualify for an exception. The same will apply if you are carrying a higher than normal debt ratio due to taking time off work after your baby was born or taking on a new dependent.

Down Payments

If you have an excellent credit rating, lenders will practically beg you to take their money. In fact, you will find that there are no shortage of no down payment (0% down) auto loans that are available for those with near-perfect credit. Of course, no down payment makes for a great offer, but you need to read between the lines to ensure the loan has no unattractive terms.

While no down payment car loans are great, you should be a little more cautious about no-interest deals. If you find a vehicle available at 0% APR, the dealer probably marked the price up to cover your interest premiums upon purchase. This is how the vehicle gets sold under financing without any interest applied. If you are okay with a nominal interest rate or plan to pay the balance off early, negotiate a discount instead of the 0% interest rate.

Best Online Auto Loans

If you are looking to finance a new car, you might want to consider looking for an online lender. Opening up the door to prospective lenders outside of your city exposes you to a whole new world of opportunity. You might get a better interest rate, monthly premium, or more preferable loan terms as a result.

Below are some of the best auto loan offers.

New Cars Plus – New Cars Plus is more than just a car loan matchmaker; this website scans auto deals across the country to find you the best price on the vehicle you want to buy. After you are linked with your preferred vehicle’s best deal, you will get presented with a car loan quote finder. This will match you with an auto lender that will approve you, whether you have perfect credit or charge-offs or worse on your file.

Blue Sky Auto Finance – Blue Sky Auto Finance is an auto loan portal website, meaning it links you to legitimate car loan providers based on your entered information. You will get matched up whether you have good or bad credit, and you can get rates as competitive as 2.99% APR on a 60-month new car loan. This is a legitimate company that has maintained an “A” Better Business Bureau (BBB) rating. The business was first ‘BBB accredited’ in 2004 and has continued to act in good faith ever since.

Capital One Auto Finance – Capital One Auto Finance is the Web’s most trustworthy car loan provider. This service is run by Capital One, one of the largest players in the credit card industry. While qualification requirements are more strenuous than what you will find from the other sites listed here, it’s worth it if you have excellent credit. Capital One offers auto financing at rates as low as 1.99% APR on loans 5 years or less. You can apply online and receive your approval or rejection within minutes. If approved, you can print your confirmation paper and visit one of more than 12,000 nation-wide car dealerships to seal the deal.

More Ways to Save

You can also find many great third-party extended warranties for your vehicle purchase. This is perfect when buying a model from a dealership that’s a few years old and running out of coverage. The warranty terms will vary, so you have to choose the right service provider; listed below are some of the best auto warranty companies.

A Plus Auto Warranty – A Plus Auto Warranty is an easy-to-understand extended coverage service that protects vehicles dating back as far as 1987. The policy allows for an unlimited number of claims to be made. The coverage is bumper-to-bumper, and you have full say over where the vehicle gets repaired. You can fill out the online form and receive a free quote for your vehicle’s extended warranty.

Not sure about extended auto warranties? Read Consumer Report’s analysis to get complete!

Best Loans is Alaska

Best Loans is Alaska