One of the most difficult things to figure out is how many credit cards you plan to have when building your credit. This is a decision that must be made ahead of time — even if you’re not planning to apply for all the cards right away.

We will explain all the different ’cause and effect’ scenarios that come about when managing the number of credit cards you own.

The Cost of Insufficient Credit

The average American’s credit score is 706 as according to our study.

A diminished score makes borrowing difficult. Worse still, any borrowing terms that are extended are often expensive with high-interest rates. These high rates represent the risk associated with a borrower who doesn’t enjoy a good credit profile.

Nearly every American will need to borrow for large purchases throughout life. The most notable of these expenses is a home.

Consider the difference in a monthly mortgage payment when an interest rate is just 1% greater.

On a hypothetical $200,000 mortgage with a 30-year fixed term, an interest rate of 4% will require a $954 monthly payment. Now, imagine you hold a lower credit score, your interest rate is 5%, and the monthly payment is $1,073 yielding a total finance charge of $149,000. This is $35,000 in extra financing charges over the mortgage life because of a mediocre score.

The above example assumes a mortgage can be obtained. In many cases, the hopeful homeowner doesn’t have a solid enough credit background to earn a mortgage at all. This is a genuine problem for many of us.

Even worse, this trend is growing at an alarming rate.

The Urban Institute conducted a broad study on this epidemic. Their findings underscore the problem: “denial rates for applicants with less-than-perfect credit have risen substantially, from 25% in 2004 to 43% in 2013.” How do we fix this? We fix it by improving our credit.

Many falsely assume that little or no borrowing with credit cards represents solvency and thus increases a credit score. However, the fact is that no credit history is bad credit history.

Good credit scores result from two actions (a) borrowing and (b) repaying at regular intervals on time. Given this fact, is it wise to boost a score with more borrowing and more repayment?

The answer. Perhaps the consumer has the ability and responsibility to repay. How do we know when more credit cards are the answer and how many are enough? Read on, and we’ll answer.

When to Choose More Credit Cards?

Deciding to use a credit score should be the result of one of (or both of) the following goals:

- To increase your credit score.

- To save spending (e.g., points, cashback, etc.).

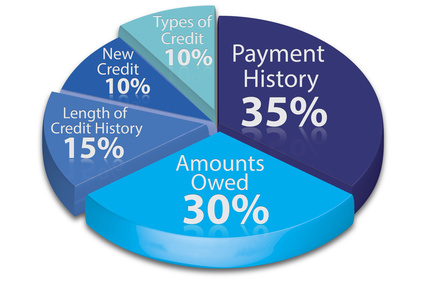

If your goal is to increase your score, opt for more cards. The number of credit cards in your name will not significantly impact them. The factors influencing your credit score include things like:

- Payment history

- Debt owed

- Length of credit history

- Recent credit

- Type of credit

A strict card count doesn’t apply here. Furthermore, those needing help with their credit score are likely not skilled at using one responsibly. Adding more cards to the mix will not help the situation. The reporting agencies are focused on your behavior as a consumer, not necessarily your ability to obtain a credit card.

Today, even those with a weak score can get their hands on a credit card, many cards in fact. This makes sense; credit card companies are eager to enable the wild spending of someone who will generate late payment fees and excessive interest rates.

But building credit is a long, multi-leveled game.

More cards make the game more difficult as there is more to manage. More invoices, varying terms, and different reward plans make the card’s choice in a specific spending scenario onerous.

When a consumer gets a new credit card, the score can drop slightly. This effect is often short-lived but worth considering. This outcome is even more pronounced when a user engages in “credit card churning,” the practice of routinely opening and closing accounts.

All financial goals are achieved with a long-term commitment. There are no shortcuts. The achievement of a superior score comes from playing the game, not attempting to gain the system. As a result, your decisions should be focused on a forward-thinking mindset.

With these considerations, one must ask, “Is there any reason to own more credit cards.” The answer is yes, under specific circumstances. Primarily this is a wise decision for those with respectable credit and responsible repayments. Let’s look at how multiple card ownership can be used by those seeking to rebuild their credit.

As explained above, the total debt owed is a major factor determining your credit score. Each with a significant balance, holding several cards can boost this metric. Each new card’s addition grants the user an incremental increase in their credit limit. The result might be an improved debt-to-credit ratio. This ratio is expressed like this:

Total Debt / Total Credit Limit

More cards will increase the bottom number (Total Credit Limit) faster than the top number. This is a way to drive down the total percentage quickly. The result is a superior credit score.

Take caution: engaging in this strategy is dangerous for those without control of their spending. If you take on a higher credit limit as a license to spend more, the top number will grow, thereby increasing the debt-to-credit ratio, which is only detrimental to your credit score. Also, your credit score drops (approximately 5 points) with each “hard pull” (hard inquiry) of your credit report, but it’s a necessary evil.

With discipline, this method can make a substantial positive impact on your credit score. For the irresponsible, it is disastrous. Make sure you know which of these two you are before you attempt. In the short run, it may be best to take a shortcut and request an increase to the line of credit already offered by an existing credit card.

Those with superior credit may also benefit from more cards to capitalize on differing benefits. Most credit cards are optimized for one spending category.

Consider juggling these cards for these spending habits:

Groceries: AMEX Blue Cash Preferred

Cash Back: Citi Double Cash Card

Travel: AMEX Starwood Guest

When to Limit Your Credit Card Count?

While closing a credit card account can be a commendable attempt to curb spending, there are drawbacks. The primary problem is the inverse of the debt-to-credit metric discussed above. Closing cards will reduce your credit limit, thereby adversely impacting your credit score. The only way to mitigate this is to simultaneously reduce your outstanding balance, which is a troublesome goal.

Closing Some of Your Cards

Shutting down some of your cards can be a good idea if your spending is out of control. The reality is that most people will greet an increased credit limit with more spending. Therefore a reduced credit limit will limit your spending.

But when willpower alone doesn’t work, it is best to close the door. This resists temptation and simplifies the task of managing your credit. While the short-term result may be a reduced credit score, the long-term will be better and less expensive.

Dropping the Annual Fee

Other savings come with a reduced card count. Approximately 25% of credit cards have an annual fee. The median fee is $50. Over an array of cards, this fee can add up. While this is a small cost related to interest payments, limiting your wallet’s cards is another reason. In some cases, the little piece of plastic in your pocket might be leaking up to $500 a year out of your account. Those with many cards often forget they have annual fees to pay. These fees are only worth the money if the card delivers something greater in the way of cashback or rewards.

Dealing with High APR Cards

A high APR is a strong argument for closing a card. This is a cost that will dwarf the annual fee problem. If credit cards have enabled excessive spending habits, you’re almost certainly paying for this recklessness in the form of a higher interest rate.

The current 3-month trend of fixed-rate credit card APRs is 11.06%, according to analytics on Bankrate.com. Variable rates are much higher, with a 3-month trend reaching 16.05%.

Consider closing the account if you’re experiencing rates above this and cannot negotiate a better rate. The benefits of various reward point plans and cashback offers will never outpace this expense.

What Happens When You Close a Card?

Closing a card will not erase your history.

If payments to a card have been late and irregular, closing the card will not make this disappear. FICO will still fold this data into the final credit score. However, as time passes, the poor history’s impact with the closed card will lower.

When choosing to close a card, consider starting with the one that has the lowest credit limit. Again, the short-run outcome of closing a card is negative. When you decided to reduce your total credit card holding, you’re engaging in a prolonged attempt to improve your score.

However, the short-term problems of closing a card can be limited by selecting a card that represents a lesser portion of your total credit limit.

Budgeting for a Balanced Approach

Time to get down to the answer. How many credit cards should you have? Most consumers can meet all their needs easily with four cards.

This allows a user to leverage benefits associated with the four categories that form the core of spending: groceries, gasoline, travel, and all-around cashback on total spending.

All consumers spend within these categories. By selecting four cards, each consolidates its rewards on one of these categories, and you can experience ample savings across nearly all your annual spending.

The Concept of Diminishing Returns

The concept of diminishing returns applies here. At a certain point, another credit card will not provide added value. The total credit limit offered by an array of four cards is high enough to enable a great debt-to-credit limit even when you are a frequent spender. If you select cards with high limits, this effect is even greater.

Four cards usually work well because it offers the rewards and credit benefits and a manageable amount. There are limits to the values we can keep coming into our heads. Using more than four cards will exceed your mental bandwidth. This leads to late payments, confusion over limits, difficulty in leveraging benefits, and a higher annual fee.

Take a Look at Your Budget

Why is this an important practice? The best place to start building your credit card lineup is to review your budget carefully. This will immediately illuminate the bigger areas of your spending.

Additionally, It allows you to use a tiered approach.

Tier Your Credit Cards by Budget / Spending Habits

This means you select your first credit card based on your budget’s largest sending category. This first card will become the most active one in your collection and represent the strongest potential benefit.

For many, grocery spending is the largest budgeted category applied to a credit card. The AMEX Blue Cash Preferred card (listed here) offers the best rewards (6% cashback on groceries) on this kind of spending.

A card promising incredible rewards for travel is of little use to a family man with two young children at home. We can often be drawn to the promotional aspects of a high annual rate card with no value given the stage of life we’re experiencing.

Consider including at least one card in your arsenal that can be characterized as a low-interest card. This can be a valuable addition for all the spending that doesn’t fit into the common reward categories.

Some examples include:

Citi Diamond Preferred

21 month 0% APR, no annual fee.

Chase Slate

15 Month 0% APR, no annual fee.

Citi Simplicity

No late fees, no penalty rates, no annual fee.

No matter which cards you choose, be sure they all meet some basic requirements, including:

- Low or no annual fee.

- Substantial credit limit.

- Low APR relative to the national average.

- No late fees.

- Best class offer for a specific spending category.

Finally, please do the math; it’s surprising how often this is looked over.

When reviewing your annual spending, pay close attention to how the credit cards will defray your costs. If your annual grocery spending is $6,000 and your card offers 6% cashback on this category, your total saving will net out to $261 after accounting for the $99 annual rate.

This means your effective cashback rate at the grocery store is actually 4.35%. If another card offers 5% cashback on this category with no annual fee, the choice is simple.

Tricks for Discussing with Credit Card Companies

The mere fact that you have the option to negotiate with a credit card company is a revelation for many. To start, be sure you fully understand your goal. For the reasons outlined earlier in this article, you may wish to increase your credit limit. Perhaps, as a long-time customer with excellent payment history, you want the annual fee waived. Focus on one goal that will make a difference.

Stay on message when speaking to the credit card representative.

Please don’t fall into the trap of negotiating with yourself by explaining why they shouldn’t meet your request. State only the reasons why they should help. Credit card companies understand one thing above all else; it is much easier and less costly to keep a customer than acquire a new one. This is especially true of a good credit card customer.

You can negotiate more than once but be sure to make your biggest request your first. Upon making your first request, you can send the message that this is the first time you’ve asked them for anything. This is particularly effective when you’re requesting a customer that has displayed a good payment history.

Be ready to walk away. The credit card company will initially push back on nearly any request. Your final leverage will be to close the account, walk away, and step into a new relationship with the competition. Make this leverage real by preparing to make good on this promise.

Thousands of credit cards are available to you. If your request goes unheard, you can find another offer that provides what you’re looking for. Have this offer in front of you when calling your credit card company. It will help prove to the representative that you’ve done the research and know your next step.

Finally, remember that timing matters. A call at 10:00 am on a Tuesday is likely best. The headache of Monday has passed, and by 10:00 am, the caffeine has taken effect. Later in the day, the representative has waged war with dozens before you and is less willing to offer a sympathetic ear to your request.

Ways for Any Consumer to Save Big with Credit Cards

Embrace credit cards. Live and breath them but do so responsibly. The competitive landscape in the credit card world provides numerous benefits to you. Like a Swiss Army knife, you need to know when to apply the right tool.

Many are unfamiliar with the car rental insurance available through many credit cards. Use this to your advantage. Some cards will also offer extended warranties of up to 1 year on purchases. This can be valuable with bigger ticket electronics.

While many cards offer points and cashback on purchases, some cards have varying points for purchases at different retailers. For example, one credit card may offer 3 points per $1 spent at Best Buy, while 6 points are offered per $1 spent at a retailer like Target. Researches if the points differ based on the retailer and spend accordingly.

Summarizing a Strategy

Take a full inventory of the cards you own and their respective benefits and fees. Next, take the time to list your annual total spending among all categories. Compare how your existing credit cards reflect your spending habits. You’ll almost certainly learn that your cards are not aligned with your spending. This is where the real research begins.

Try to stay within the limit of four cards. Having more is not necessarily a problem but be sure you have a good reason to hold more.

Suppose your card benefits don’t reward you for the kind of spending you’re accustomed to considering swapping out a card. You want cards with rewards that will yield value even as your lifestyle changes. If your ditching a card for any problem that can be solved with a well-timed call to the credit card company, be sure to exhaust this strategy first.

Plan Your Spending Around Your Cards!

Favor retailers that have credit card perks that favor you. Take the time to review all the numbers to ensure the net savings among all your cards far exceed the costs and fees associated with owning them.

Don’t be swayed by perks that will have little value. Balance transfer benefits are of little use to most consumers. Understand the risks involved. A poor credit score begets a worse credit score.

This can easily become a credit score-free fall. Making broad changes to your cards will not yield great value in the short run. Keep in mind the long-game nature of credit card ownership to gradually build your score.

While each consumer has different spending habits, success’s main concepts are universal. The key is organization and a careful approach characterized by responsibility.

You are the single greatest asset in your drive to achieve value from credit cards. The better you manage your cards, the more empowered you become as a consumer, and the greater your life savings will be. You will be able to command more perks, better deals, and most importantly, an excellent rate on all borrowing.

So you know what needs to be done; it’s time to get credit strong!

Best Loans is Alaska

Best Loans is Alaska